Micron (MU) stock trades at $323.21 following a record-breaking Q2. Analyze the “why” behind the price action, from HBM4 mass production to the $25B AI infrastructure bet.

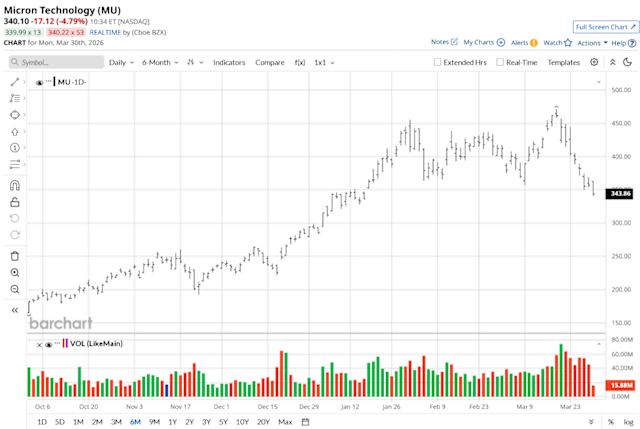

As of the closing bell on March 31, 2026, Micron Technology (NASDAQ: MU) sits at $323.21, reflecting a modest intraday gain of 0.44%. While the daily ticker shows stability, the month of March has been a high-pressure gauntlet for the memory giant. After touching a 52-week high of $471.34, the stock has retraced significantly, leaving investors to wonder: is the AI memory supercycle losing its “grit,” or is this merely the foam settling?

For TechRebot readers, understanding the “why” behind this price action requires looking past the surface level of the NASDAQ and into the deep-tissue mechanics of global semiconductor supply.

1. The Blowout Q2: When “Beating” Isn’t Enough

On March 18, 2026, Micron reported fiscal Q2 results that would have been unthinkable two years ago. Revenue skyrocketed 196% year-over-year to $23.86 billion, while earnings per share (EPS) hit $12.20—obliterating the forecasted $8.79.

The “grit” of these numbers is found in the operating margins, which surged to a staggering 69%. Despite this, the stock price faced immediate downward pressure. This is the “Priced-to-Perfection” Trap: with a 340% run-up over the last 12 months, institutional traders used the record-breaking news as a liquidity event to take profits, proving that even a 682% increase in EPS can be met with a “sell-the-news” reaction in a hyper-extended market.

2. HBM4 Mass Production: The NVIDIA “Vera Rubin” Catalyst

The most significant technical news of late March is the official start of HBM4 36GB 12-Hi memory mass production. This isn’t just a roadmap update; it is a direct assault on the market share of Korean rivals SK Hynix and Samsung.

Micron’s HBM4 is specifically engineered for NVIDIA’s next-gen Vera Rubin platform. The technical specs are formidable:

- Bandwidth: More than double that of HBM3.

- Efficiency: A 20% improvement in power-per-bit, a critical metric for the power-hungry data centers of 2026.

- Inventory: Micron has confirmed that its HBM4 capacity for the remainder of 2026 is already sold out under binding contracts.

3. The $25,000,000,000 Infrastructure Gamble

Micron is no longer acting like a cyclical commodity player. Management has raised its fiscal 2026 Capital Expenditure (Capex) to over $25 billion.

This massive spend is being funneled into new “cleanrooms” and advanced lithography to meet an AI demand that Micron can currently only satisfy at a 60% fill rate. While bulls see this as a sign of a “structural growth” shift, bears worry about the Free Cash Flow (FCF) pressure. If the AI buildout hits a plateau in 2027, this $25 billion investment could become an expensive anchor. However, the recent signing of a five-year strategic customer agreement—a rarity in the memory world—provides a level of revenue visibility that historically did not exist.

4. Analyst Sentiment: The Gap Between Price and Value

Despite the recent slide to $323.21, the “Council of Analysts” remains largely undeterred.

- Stifel Nicolaus maintains a target of $550.

- HSBC recently boosted their target to $500.

- Consensus: With a forward P/E sitting at a remarkably low 6.1x estimated 2027 earnings, MU is currently trading as one of the “cheapest” ways to play the AI infrastructure boom.

The Final Takeaway

The current MU stock price is a reflection of a market struggling to value a company that is fundamentally changing its DNA. Micron is attempting to break the “boom-and-bust” cycle of the memory industry by becoming an indispensable pillar of the AI age. For the long-term observer, the volatility of March 2026 isn’t a sign of weakness—it’s the friction of a legacy industry being rebuilt for an autonomous future.